MARKETS ARE BECOMING COMPLETELY HEADLINE-DRIVEN AGAIN

The US-Iran conflict dominated markets over the last 24 hours, with oil, crypto, equities and bonds reacting sharply to every new military and diplomatic headline.

Reports suggested the US conducted fresh strikes inside Iran following Iranian drone activity near regional shipping routes. Earlier, Iranian state media floated a potential framework involving sanctions relief and restored access through Hormuz, but the White House later pushed back on parts of the narrative.

OIL IS NOW THE MOST IMPORTANT MACRO ASSET IN THE WORLD

Crude oil initially dumped below $89 as markets reacted positively to reports of a potential Iran framework, but prices quickly reversed back above $90 after fresh military escalation headlines emerged.

The current market structure shows just how fragile sentiment has become. Every escalation headline pushes inflation expectations higher, while every peace-related headline temporarily revives risk appetite. However, conviction remains weak across all major markets. Fed officials are already warning about potential supply disruptions and energy shortages if conditions around the Strait of Hormuz fail to stabilize.

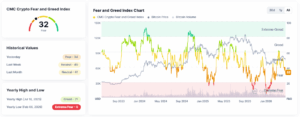

THE FEAR AND GREED INDEX IS FLASHING RISK-OFF AGAIN

The index has now dropped to 32 after sitting near neutral levels around 40 just one week ago, highlighting how aggressively sentiment deteriorated following the latest US-Iran escalation headlines.

The move also marks a sharp reversal from the yearly high reading of 71 reached during the July rally phase, while still remaining well above the extreme fear low of 5 recorded back in February.

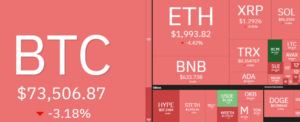

BITCOIN CONTINUES SHOWING WEAK RELATIVE STRENGTH

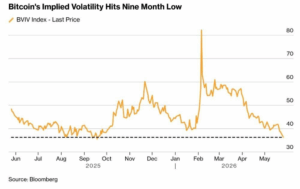

BlackRock has now extended its selling streak to eight consecutive sessions, while BTC ETFs recently recorded more than $1.2 billion in weekly outflows. Trading activity also remains near multi-month lows, with Bitcoin’s expected 30-day volatility falling toward a nine-month low as activity slows across the broader ecosystem.

Onchain demand metrics are showing similar weakness, with CryptoQuant recently flagging one of the deepest negative apparent demand readings on record, while Glassnode data points to persistent softness in spot participation and capital inflows. During the latest Iran-related escalation move, more than $260 million in BTC and ETH longs were liquidated within an hour, reinforcing how fragile leverage conditions still remain.

Ethereum also continues to lag, falling back below the key $2,000 level while ETF outflows persist. Yesterday, ETH spot ETFs recorded more than $67 million in net outflows, with BlackRock’s ETHA accounting for over $65 million of the total selling pressure. At the same time, the daily chart is now becoming oversold, with price pressing firmly against higher-timeframe falling wedge diagonal support as bearish momentum continues building.

ALTCOINS ARE STARTING TO SHOW SIGNS OF STRESS AGAIN

WLD has now fallen roughly 28% from its recent highs and is currently testing major support near its 100-day moving average around the $0.3 region.

This is becoming an important level for bulls to defend. If broader macro conditions stabilize and de-escalation headlines continue improving sentiment, WLD could attempt a recovery back toward the recent $0.41-$0.42 highs.

However, failure to hold the current support structure could expose the token to a deeper breakdown toward the $0.23 region, especially if risk appetite across altcoins continues deteriorating alongside broader market volatility.

JTO is also coming under heavy pressure, falling more than 13% today. Price is now losing the key $0.5 region after repeatedly failing to sustain momentum above recent Fibonacci resistance levels.

If macro conditions continue deteriorating and war escalation headlines keep pressuring risk assets, the current structure increasingly opens the door for a larger breakdown toward the next major support zone near $0.23.

ONDO is also starting to lose momentum after facing multiple negative catalysts simultaneously, including SEC delays around tokenized stock plans, the recent passing of the project’s founder and broader geopolitical risk-off pressure across crypto markets.

Now struggling to reclaim the key $0.41 resistance region after rejecting from the recent breakout attempt near the $0.45 area.

If sentiment continues deteriorating alongside ongoing war headlines, failure to recover the current structure could expose it to a larger retracement back toward the major support zone near $0.24.

TRUMP CONTINUES PUSHING CRYPTO BUT BTC DIDN’T CARE

President Trump released another strongly pro-crypto statement overnight, promising future digital asset legislation and continued support for the industry inside the United States. However, despite the bullish rhetoric, Bitcoin barely reacted and later continued drifting lower as traders remained focused on war escalation, oil volatility and broader macro uncertainty. The weak response increasingly shows that geopolitical and liquidity conditions are currently driving markets far more than political crypto headlines alone.

AI EQUITIES CONTINUE MELTING HIGHER WHILE CRYPTO LAGS

One of the biggest divergences across global markets right now is the growing disconnect between AI-driven equities and crypto.

Semiconductors and AI infrastructure continue attracting enormous institutional flows:

• Micron is up nearly 1,500% in 13 months

• SK Hynix surged roughly 1,800% over the past year

• The Semiconductor Index is up more than 159% since the start of 2025

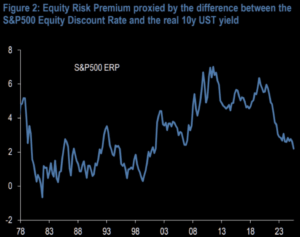

Meanwhile, the S&P 500 and Nasdaq continue trading near all-time highs while Bitcoin still remains more than 41% below its peak. At the same time, the S&P 500 Equity Risk Premium has now fallen to its lowest level in more than 20 years, approaching levels historically associated with extremely stretched market positioning.

This divergence is becoming increasingly important. Capital continues aggressively concentrating into AI infrastructure, compute and semiconductor exposure while broader crypto markets continue struggling with weaker momentum and persistent ETF outflows.

WHAT TO WATCH NEXT

Today’s biggest macro event is the April PCE inflation report releasing at 8:30 AM ET alongside the second estimate for Q1 GDP.

Current expectations:

• Headline PCE YoY: 3.9% vs 3.5% prior

• Core PCE YoY: 3.3% vs 3.2% prior

• Q1 GDP expected near 2.0% annualized again

Meanwhile, markets remain heavily focused on:

• Further US-Iran escalation or peace headlines

• Continued BTC and ETH ETF outflows

• Bitcoin’s ability to hold key support near the $72K-$74K region

• Whether altcoins continue breaking major support structures

• And if fear continues accelerating across crypto markets

TRADE GLOBAL VOLATILITY WITH BITFUNDED

With markets reacting aggressively to geopolitical headlines, volatility continues creating opportunities across every major asset class.

- Access funded accounts

- Trade crypto, commodities, indices and equities

- Scale positions responsibly during volatile markets

START TRADING WITH BITFUNDED

THE BITFUNDED TEAM